The latest RBA pause and your property plans

Last week, Tuesday 4th April 2023, the RBA board decided it was time for a pause, but of course Dr Phillip Lowe, governor of the RBA, left the door wide open for further interest rate movement.

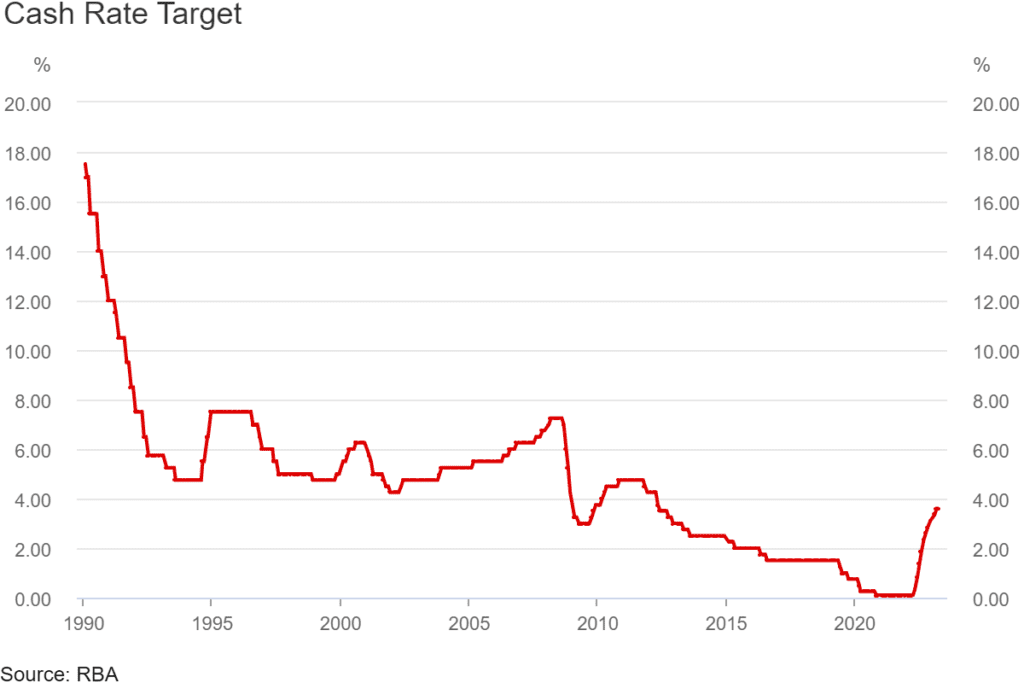

As shown in the following graph, the cash rate is now at 3.6%, marginally higher than this time 10 years ago.

Right now, forecasts and predictions are plentiful. Toss a coin and I’m pretty sure you’ll have the same chance of getting it right as those making predictions and forecasts.

Truth is no one knows. Even those who are paid the big bucks, like the RBA's governor million-dollar man Dr Phillip Lowe, seldom get it right!

If you are making financial moves based on short term noise, and/or based on forecasts and predictions, your chance of success will be slim.

The facts right now...

Inflation is slowly reducing, after a peak of 8.4% in December 2022, now sitting at 6.4%. The RBA board believes that the central bank's inflation target of 2-3% will not (likely) be achieved for another two years.

Interestingly, money markets are pricing in a very "slim" chance of further rate increases - as well as pricing in a strong probability of a 25 bps decrease before the year 2023 is out. Time will tell I guess!

The day after the pause announcement, Wednesday 5th April 2023, the RBA governor addressed the National Press Club in Sydney, saying that the RBA was “looking very carefully” at the flow of money into mortgage offset accounts.

“This is the way that people with a mortgage save; the money goes into the offset account. And we’ve noticed, in the recent few months, that the flow of money into these offset accounts is slowing. That suggests that people don’t have as many free cash resources as they previously did, that’s a really important source of information,” Dr Lowe said.

My read on this is that the RBA is well aware that home loan customers are draining their cash buffers right now to meet higher loan repayments, which will be further exacerbated once the anticipated fixed rate mortgage cliff starts to eventuate.

What does the latest RBA pause mean for your property plans?

The latest pause by the RBA is a positive step towards market sentiment - and sentiment is a key driver of property values - speaking from experience.

Given the rate hikes experienced within the last 12 months, and now a pause, you may be confused about your property plans and related timing.

Perhaps you are considering upgrading your family home, knowing that this is important for your growing family over the coming years, or changing suburbs to align with your desired lifestyle.

Or, perhaps you want to buy an investment property - or accumulate more property - as you know this is important as you work towards a more secure financial future.

You may even be contemplating getting a foothold on the property ladder as a first home buyer.

If any of the above resonate with you, you are probably confused about the timing of your next property move - if you are like most people. Perhaps timing the market is your strategy, thinking the market has further to fall.

Here's a strong tip from experience with over three decades of property investment success. Timing the market will cost you as no one rings the bell when the market has peaked, and no one rings the bell when the market has bottomed.

COVID is a case in point, where many property buyers sat on the sidelines thinking the market would fall further, to later discover that they priced themselves out of the market from exorbitant price increases. Or even from their inability to qualify for finance as the interest rate spikes had suppressed their borrowing power by up to 40%.

7 facts you should consider when contemplating the timing of your next property move!

When considering the timing of your next property move, it's important to consider the facts and to lead by strategy, as opposed to speculative guesses and wild forecasts.

Here are the facts which hold all the clues as to why right now could be the best time for you to make your next property move.

- The cash rate is now at 3.6%, which is only marginally higher than this time 10 years ago. This highlights the fact that the historical low cash rate over the last few years was temporary - driven by the pandemic.

- House prices are now at intrinsic value when compared to the runaway prices we saw post lockdown. For example, Melbourne's median house price now sits at ~$897k when compared to ~$1m this time 2 years ago (source: www.theurbandeveloper.com)

- Many developers and builders have been squeezed out of the game from surging labour and material price increases - Porter Davis was sadly the latest statistic. This means more and more people are having to rent, increasing the demand for rental accommodation, which will ultimately increase the demand for more housing. As demand for housing increases, so do property values!

- Stock levels have been running thin for quite some time, in particular for quality family homes. This is expected to continue especially given the expected surge in demand for quality homes - in light of point 3 above.

- Melbourne auction clearance rates have remained healthy in the high 6's and even early 7's - even as interest rates spiked over the last 12 months.

- Australia is about to welcome ~1.3million immigrants over the next 2 years, with ~300k this year alone (based on Treasury forecasts). This will put enormous strain on the rental market, as well as housing prices, as the demand for property is likely to surge. With supply already low and demand set to increase, property prices can only head in one direction - and this is up!

- APRA has maintained a 3% mortgage buffer knowing that the emergency rate cuts, driven by COVID, would not last. It is likely that APRA will reduce this buffer back to a normal level knowing that interest rates have (likely) peaked in this cycle - or are very close to peak.

When contemplating your next property move, I recommend you beat to the march of your own drum and make your property and financial moves based on facts, ignoring sensationalised headlines which are there purely for click bait.

Your next property move should be based on your own lifestyle choices, your affordability, and of course your borrowing capacity.

Time in the market trumps timing the market, period! Play the long game and you can't go wrong. Speculating on interest rates and on property values will cloud your judgement when it comes to your next property move.

I hope that my blog today helps you in some way, and if we can help you buy your next property based on strategy and success, please contact us as we are ready and willing to assist.

Important information: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. For this reason, any individual should, before acting, consider the appropriateness of the information, having regard to the individual’s objectives, financial situation and needs and, if necessary, seek appropriate professional advice.